How Federal Employees Can Plan to Retire on Time

By Clear Insight Wealth Management

As a federal employee, you enjoy unique perks and benefits, but perhaps the most valuable is the potential to position yourself for strong future financial stability. Unlike many people in the private sector, retiring after 30 years of service is a real possibility. However, simply qualifying for an earlier retirement doesn’t guarantee a smooth transition. Without thoughtful planning and strategic financial management, retiring comfortably can be as challenging for federal employees as it is for anyone else.

We’ve witnessed how lack of preparation can lead people back into the workforce after trying to retire, and we’re here to help you avoid that. Let’s talk about the steps you can take to make on-time retirement a reality.

Know Your Retirement Age

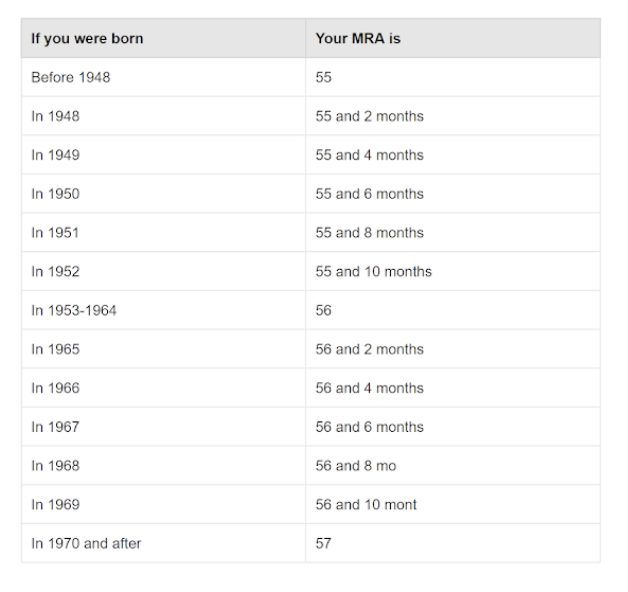

One of the keys to retiring on time is maximizing your retirement benefits. When you retire and how long you have been in service will greatly affect the benefits you receive. If you retire before you have reached your minimum retirement age (MRA) or before you have completed enough service, you will not be able to maximize your benefits. The following chart shows your minimum retirement age:

To receive full benefits, you must either have 30 years of service and reach your MRA, or have 20 years of service and be age 60 or older. If you have between 10-30 years of service, you are allowed to retire at your MRA, but your benefits will be reduced by 5% a year for each year you are under age 62. For example, if you retire at age 56 with 19 years of service, your benefit will be reduced by 30% (5% for each of 6 years). However, if you work 4 more years and retire at age 60 with 23 years of service, you will receive the full benefit.

The amount of benefit you receive will affect your ability to retire successfully (i.e., having enough money to live on without going back to work). It is important to strategically balance your years of service and retirement age in order to receive a high enough benefit to support you during retirement. Sometimes simply working one or two more years can make a big difference in your benefit amount.

Keep Your High-Paying Job a Little Longer

Another factor in your benefit calculation is your salary. Under FERS, your pension benefit is calculated as:

(average of 3 highest years’ salary) X (years of service) X (pension multiplier)* = (annual pension benefit)

*The pension multiplier depends on your years of service and age at retirement, as discussed above.

If your salary significantly increases shortly before retirement, working a couple more years may be well worth it. Let’s say you plan to retire at age 60 with 30 years of service. One year prior, you go from earning $100,000 as you did for the previous 2 years to $120,000. If you retire as planned, your pension benefit will be:

$106,667 X 30 years X 1.1% = $35,200

If you decide to stay in that higher-paying job for two more years, your pension benefit will be:

$120,000 X 32 years X 1.1% = $42,240

Staying in the higher-paying job for at least three years to increase your benefit calculation can make a big difference in retirement. In our example, it is a $7,040 difference per year. Over a 20-year retirement, that comes out to $140,800.

Take Advantage of Your TSP Match

In addition to your FERS pension, as a federal employee, you have access to the Thrift Savings Plan (TSP). Instead of getting a promised pension amount, what you get out of it is a combination of what you put in and how you invest it, much like the popular private-sector 401(k) plan. It is your choice whether or not to contribute to the TSP and how much you put in it.

To build up the most funds for retirement, you need to contribute up to your agency’s match. Receiving a matching contribution from the government is essentially an immediate 100% gain on your money. Your agency matches your contributions up to 5% of base pay, so you should contribute at least that much. Contributing any less is leaving free money on the table, money that will fund your retirement.

Strategize Growth in Your TSP

On top of getting your agency match, you want to invest your TSP funds wisely. Where you put your money over a 30-year career can make a huge difference in your account balance when it comes time to retire, and it can greatly affect your ability to do so. It may be tempting to keep your money protected from the volatility of the stock market, but that also robs you of the opportunity for your money to grow along with the stock market. Without that growth, you may not have enough funds to retire on time.

Your TSP investment choices should reflect your age, goals, and risk tolerance, as there’s no universal strategy that fits everyone. Partnering with a financial advisor can be a smart move—not only to diversify your TSP portfolio but to build a comprehensive retirement plan tailored to your needs and timeline.

At Clear Insight Wealth Management, we collaborate with our clients to craft personalized retirement strategies that bring confidence and clarity for the road ahead. Our goal is to help safeguard your future with customized, partnership-driven plans, equipping you to navigate today’s complex financial landscape.

To set up a Get to Know You meeting, schedule online here.

About Clear Insight Wealth Management

Clear Insight Wealth Management is a wealth management firm for military families, government employees, and small business owners looking for a clear path to living their best lives. The firm’s team of CERTIFIED FINANCIAL PLANNER® professionals and a Certified Public Accountant is committed to helping clients navigate the complexities of today’s financial landscape by providing realistic advice, a distinct plan of action, and helping them progress toward their goals. With an emphasis on relationships and services including financial planning, investment management, and tax planning & preparation, Clear Insight Wealth management helps clients build—not just maintain—wealth in Spokane, Washington, Tyson’s Corner, Virginia, and across the United States.